The death of the European Banking Union

This was the title of a note by Louis Rouanet published on 03 July 2017 as Mises Wire on mises.org. He argued that the bail out of two Italian banks, Veneto Banca and Banca Popolare di Vicenza, in June 2017 by the Italian government gave the deathblow to the European Banking Union, which become effective in November 2014 with the launch of the Single Supervisory Mechanism. In this note I will show that he was right as the correlation between risk premia for sovereigns and banks has sharply increased since then to the high levels observed before the start of the Banking Union. It was exactly this “disastrous sovereign-banking nexus, in which shaky bank balance sheets degrade the solvency of their sovereigns, and vice versa”, that the Banking Union was aiming to sever (Weidmann, 2013). The budget plans of the new Italian government therefore have the potential to trigger a new financial crisis.

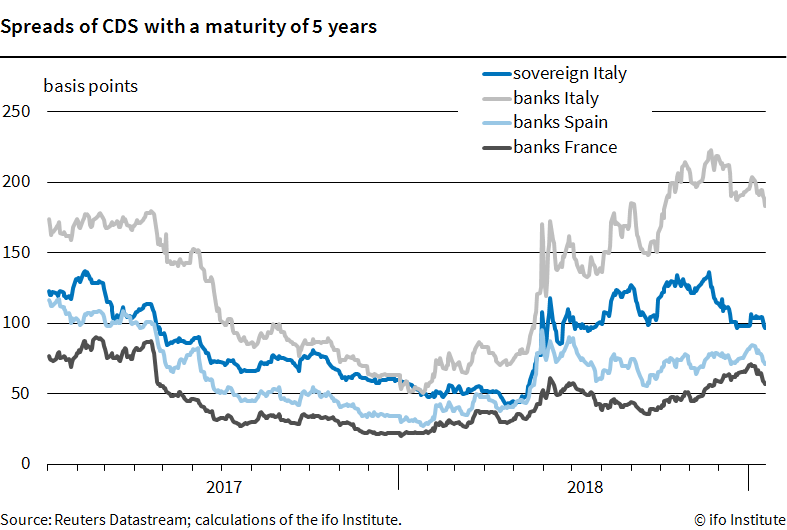

These plans and the associated dispute with the EU Commission have led to a significant increase in risk premiums for Italian debt instruments. While the yield gap to German government bonds with a residual maturity of 10 years was relatively stable at an average of 1.3 percentage points between January and April 2018, it rose sharply on 18 May 2018, when the coalition agreement of the current Italian government was signed, and reached its temporary high of 3.3 percentage points on 20 November 2018. Since then, after the Italian government has signaled its willingness to make changes to the draft budget, risk premiums have been starting to fall, but the levels reached until recently are still higher than before the elections. The premiums of credit default swaps (CDS), which are traded over-the-counter and serve as a measure of the probability of default of a specific debtor within a specified period, show a very similar trend. For the five-year protection against insolvency of the Italian government, they rose from an average of 52 basis points in the first four months of 2018 to 136 basis points on 20 November (see Fig. 1).

One of the main creditors of the Italian government are Italian commercial banks. At mid-2018 they held about 18% (353 billion euros) of the outstanding amount of government securities. As the rise in yields forced creditors to book losses on the Italian sovereign bonds, which reduced the banks’ equity and thus increased their probability of default, risk premiums for lending to Italian banks increased at the same time as risk premiums for the Italian sovereign rose. Since the beginning of the year, the average premium required by investors to insure loans to Italian banks for a term of five years has quadrupled.[1] But also foreign commercial banks hold a significant proportion of Italy’s public debt. In mid-2018, the claims of French and Spanish commercial banks on the Italian State amounted to 55 billion euros and 41 billion euros respectively. Since May 2018, their risk premiums have about doubled as a result of the slump in prices of Italian government bonds.[2]

Fig. 1

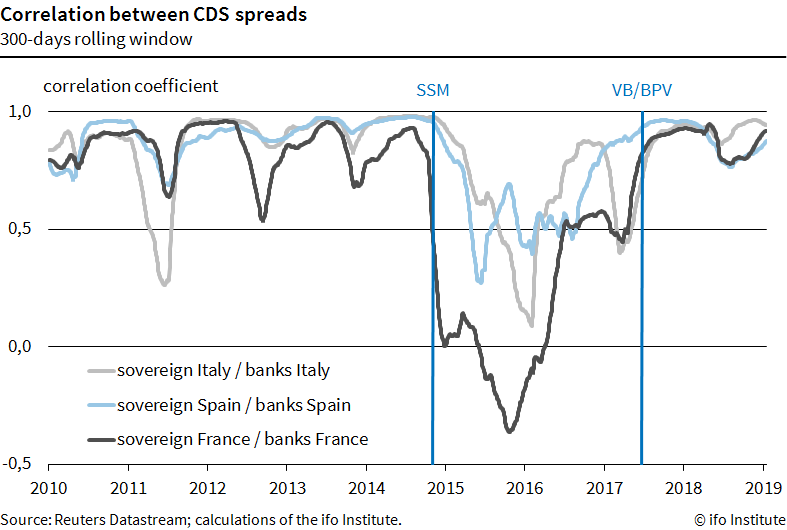

An escalation of the budget dispute thus not only endangers the stability of the Italian banking system, which is already weakened by its above-average share of non-performing loans in the total loan volume. It may also be transferred to the banking systems of other countries which hold claims against the Italian government. If banks get into financial difficulties, the probability increases that the risks associated with a bank rescue may be transferred to the state in which the banks are located. During the global financial and euro crisis, it was precisely this vicious circle that led to an escalation of the European sovereign debt crisis. The banking union, which effectively started with the ECB’s takeover of the Single Supervisory Mechanism (SSM) in November 2014, was supposed to sever the nexus between the default risk of sovereigns and commercial banks. In particular, the losses arising from the liquidation of a distressed bank should in future be borne primarily by the shareholders and creditors of a bank and no longer by the government and thus by the taxpayers. The significantly lower correlation between the CDS spreads immediately after the SSM came into force suggests that this project initially appeared credible (see Fig. 2).

Fig. 2

However, the pickup in synchronization since 2017 indicates that this credibility has been gambled away. The liquidation of the two Italian banks Veneto Banca (VB) and Banca Popolare di Vicenza (BPV) in June 2017, for whose liquidation the Italian government provided aid in the form of state guarantees (12 billion euros) and cash injections (5 billion euros) (European Commission 2017), is likely to have contributed significantly to this. Although these measures did not conflict with the rules of the Banking Union, since the Single Resolution Board of the European Banking Union decided to delegate the responsibility for winding up of the banks to the hands of the national supervisors due to the non-systemically relevant size of the two banks (Single Resolution Board, 2017), they still contradicted their spirit. The case shows once again that the rules drawn up by the European community of states to achieve a more stable monetary union offer sufficient loopholes for the objectives associated with the rules not to be achieved.

[1] The spreads of CDS for Italian commercial banks is calculated as the weighted average of CDS spreads of UniCredit, Intesa Sanpaolo, Banca Monte dei Paschi di Siena, Unione di Banche Italiane and Mediobanca, with the value of total assets at the end of 2017 as weights.

[2] The spreads of CDS for French commercial banks is calculated as the weighted average of CDS spreads of BNP Paribas, Crédit Agricole, Société Générale and Axa Banque. For Spain it is Banco Santander, Banco Bilbao Vizcaya Argentaria, Banco de Sabadell and Bankinter.

References

European Commission (2017), State aid: Commission approves aid for market exit of Banca Popolare di Vicenza and Veneto Banca under Italian insolvency law, involving sale of some parts to Intesa Sanpaolo, press release, 25 June.

Single Resolution Board (2017), The SRB will not take resolution action in relation to Banca Popolare di Vicenza and Veneto Banca, press release, 23 June.

Weidmann, Jens (2013), Breaking the sovereign-banking nexus, Financial Times, 01 October.

Timo Wollmershäuser: The death of the European Banking Union, EconPol Opinion 15, February 2019.