Impact of the Covid-19 Lockdown on Firm Liquidity and Solvency: The Case of France

The confinement measures introduced in several countries to fight the Covid-19 pandemic have imposed a high toll on many economic activities. The risk is that, without government intervention, the drain on liquidity determined by running fixed costs and no revenues will make several firms insolvent, forcing them to leave the market.

The OECD has recently investigated the issue looking at firm-level data for 16 European countries. It finds that shock determined by the lockdown may lead almost 40% of nonfinancial firms to experience liquidity shortfalls.[1] Government intervention, on the other hand, can limit this number to 10%.

Yet, is it worth it?

In this post we exploit recent evidence on French firms recently published by the OFCE-SciencesPo, to discuss the policy options facing European governments and the broader implications of firm exit for competitiveness.[2]

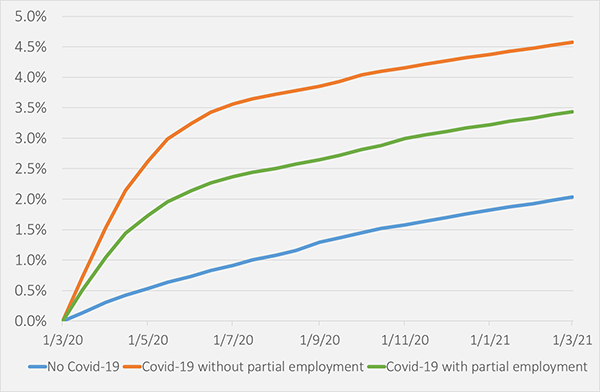

Using data on a large number of French firms, we simulate the impact of the lockdown on their balance sheets, to estimate the share of companies facing liquidity or solvency issues. The main results from the simulation exercise show that the lockdown has profound effects on firms. As shown in Figure 1, the fall in revenues due to the lockdown and the presence of fixed costs that do not immediately adjust to the lower level of activity, take a heavy toll on nonfinancial firms. We estimate an increase in insolvencies by almost 80% (from 1.8% in a No-Covid scenario to 3.2%).

The simulation exercise also suggests that the impact of the crisis varies greatly by industry, with hotels and restaurants, household services, and construction being the most vulnerable sectors. Manufacturing, on the other hand, seems much less affected. There is also large heterogeneity by firm size: insolvencies are more diffused among micro- and large firms, the former having smaller buffers of liquidity to weather the crisis, the latter being more leveraged and thus facing larger fixed (financial) costs. On the other hand, SMEs and mid-sized companies appear more resilient.

Figure 1: Cumulative share of insolvent firms under different scenarios

Another important lesson from the simulation is that the furlough scheme (activité partielle) put forward by the French government (as well as by other European countries) to avoid mass unemployment is very effective in limiting insolvencies. By taking part of the labor costs off firms’ balance sheets, the measure increases the speed of adjustment and limits the drainage of liquidity. Figure 1 shows that, without such a device, the share of firms that risk becoming insolvent by the end of the year would be more than 1 percentage point higher (4.4% instead of 3.2%), which means some 12,000 additional firms.

The question remains, however, as to whether avoiding insolvencies is a meaningful policy goal. After all, if the market correctly separates the wheat from the chaff, policymakers should foster creative destruction simply by promoting the reallocation of resources towards their most productive use. On the contrary, if the selection mechanism performs poorly, so that the Covid-19 shock pushes viable and efficient companies out of the market, it makes sense to intervene in order to keep these businesses afloat.

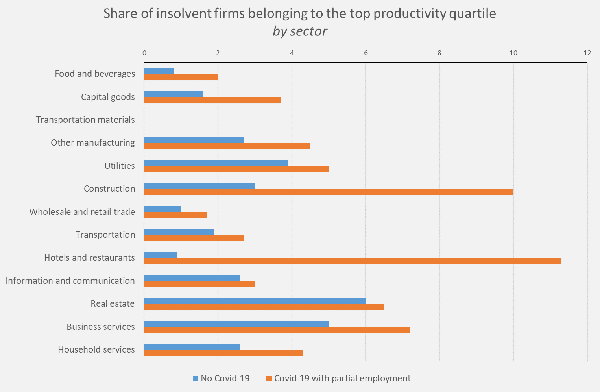

The simulations suggest that, while selection works well in the No-Covid scenario, it becomes much less efficient in the wake of the lockdown. To assess the performance of markets, we look at the share of insolvent firms that belong to the top quartile of productivity (Figure 2): perfect market selection implies that this fraction should be close to zero. We observe that in some sectors, most notably the hotel and restaurant industry and construction, the share of highly productive firms that become insolvent skyrockets, jumping from 1 to 11% in one case, from 3 to 10% in the other.

Figure 2: Share of insolvent firms coming from the top quartile of the productivity distribution.

Note: in Transportation Materials all insolvent firms come from the bottom part of the productivity distribution under both scenarios.

The weakening of market selection provides a rationale for public intervention aimed at sustaining viable but illiquid firms during the crisis. Back of the envelope estimates imply that, in the case the French government wanted to save the firms that are pushed to insolvency by the Covid-19 pandemic the cost would be around 3 billion euros (this is the cost necessary to firms to cover their losses up to September 2020). On the other hand, a policy aimed at avoiding all insolvencies (and not just those triggered by the lockdown, which may be difficult to identify precisely), the cost would raise to 8 billion.

The practical difficulties come from the fact that policymakers may not be better equipped than the market to discriminate among “good” and “bad” firms. One possibility would be to condition any public support on the absence of any overdue payment at the beginning of the crisis, as a partial means to identify viable firms.

[1] Lilas Demmou, Guido Franco, Sara Calligaris, Dennis Dlugosch, 2020, Corporate sector vulnerabilities during the Covid-19 outbreak: Assessment and policy responses, Tackling Coronavirus Series.

[2] Mattia Guerini, Lionel Nesta, Xavier Ragot, Stefano Schiavo, 2020, Firm liquidity and solvency under the Covid-19 lockdown in France, OFCE Policy brief 76, July 6.

M. Guerini, L. Nesta, X. Ragot, S. Schiavo: "Impact of the Covid-19 Lockdown on Firm Liquidity and Solvency: The Case of France", EconPol Opinion 35, July 2020