Fiscal Rules Post-COVID: Using the Recovery Phase to Reduce Debt Ratios

The Commission has recently launched a review of the economic governance rules. One reason for this (re-)launch is that it is widely assumed that the debt reduction criterion cannot and should not be enforced when the suspension of the fiscal rules motivated by the Covid crisis ends. The main reason given is that debt levels have increased and that this makes it more difficult to reach the debt reduction target, which is one twentieth of the difference between the actual and the 60% reference value. However, this argument is wrong. The debt reduction criterion becomes easier to achieve during the post-Covid recovery phase because nominal GDP growth is higher than before the crisis, thus reducing the primary surplus required to achieve any given reduction in the debt to GDP ratio.

The 2021 Stability Programs Imply Little Improvement in Debt Ratios despite Favourable GDP Growth

The Stability Programs that Member States submit (and then agree) with the Commission contain forecasts for the main macroeconomic variable for the next 4 years, including primary deficits, the debt ratio and a measure of how strong growth helps to reduce debt ratios. A key element of the 2021 programs is that they foresee for most Member State a growth rate of nominal GDP higher than 5% until at least 2023. A high growth rate of GDP helps naturally to reduce the ratio of debt to GDP because the denominator increases.

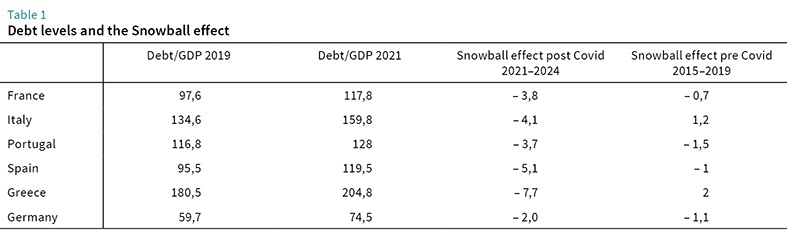

The Commission also provides an estimate of this so-called “Snowball effect”, i.e. the impact of nominal GDP growth on the debt ratio. The table below shows some of the key numbers for the larger and highly indebted member states. The debt/GDP ratio has increased in all cases (compared to 2019), most in Italy (25 points) and least in Portugal (11.2 points – less than in Germany). This higher starting level in 2021 is the basis for the argument that the debt criterion should not be reinstated. But a combination of higher debt levels and higher growth strengthens the snowball effect and makes it proportionally easier to reduce debt ratios.

This is illustrated in the last two columns which report the overall “Snowball effect” as calculated by the Commission which takes into account interest payments and the growth rate of nominal GDP A negative value implies that high growth helps to reduce the debt ratio.

The last but one column shows the average snowball effect expected over the four-year period 2021-24, which constitutes the horizon for the NGEU program. It is apparent that over the next years all the highly indebted countries will benefit from a snowball effect which is close to 4% of GDP (per annum).

Source: Own calculations based on Commission data

Comparing the last two columns one sees that the change (i.e. the difference before and after the Covid-crisis) in the snowball effect is largest for Italy where it turns from an unfavourable 1.2 to a favourable (negative) value of 4.1 for a total improvement worth 5.3 percentage points (each year). For Italy the fiscal effort to achieve the 1/20th reduction in the excess debt (relative to the 60% of GDP benchmark) will thus be over 5 percentage points of GDP lower than in the past.

The improvement in the capacity to reduce debt ratios is less impressive for most other countries which did not have the dismal growth record of Italy over the last years, but the post-Covid snowball effect would even in these cases so large that it should make it easy to satisfy the debt reduction criterion. For example, for Portugal and France, the required reduction of the debt ratio would be approximately 3 percentage points per annum (=(120-60)/20), which is less than the snowball effect these two countries can expect. The same applies to Greece, which would have the highest debt reduction requirement (7 points per annum=(200-60)/20) and the highest snowball effect (7.7 points).

All these countries would thus need not even need to run a primary surplus in order to reduce their debt ratio along the path foreseen in the present fiscal rules. The increased need for green and digital investment (also emphasized by the joint letter of Dombrovskis and Gentiloni) does not provide a counterargument because for most countries the additional investment is financed by the NGEU. There might be many reasons to change the deb (reduction) criterion, but the argument that it become more difficult to achieve a substantial reduction in debt ratio when the starting level is high, is wrong.

For the next few years, it will be easier to reduce debt ratios than before Covid.

Francesco Corti and Daniel Gros: "Fiscal Rules Post-COVID: Using the Recovery Phase to Reduce Debt Ratios", EconPol Opinion 46, October 2021.